Appearance of new digital players, the Asian market saw a new opportunity to strengthen its production capacity, and open up to new territories in the West thanks to production with a greater impact, as well as an audience more open to new content.

‘Home to 60% of the world’s population, the 4.3 billion residents of the Asia-Pacific region are contributing tremendously to the engagement with and development of online-video content and the industry on a whole. With a reported 16% growth in the industry reaching USD 49.2 billion, SVOD will contribute 50%, user-generated content-drivenAVOD will contribute 37% and premium AVOD will account for 13%. It is projected that by 2027, growth will reach USD 72.7 billion at an average rate of 8%’, Media Partners Asia says on its special report.

And adds: ‘Local content production in the APAC region is a significant contributor to increasing activity with online video, leading to mainstream distribution deals and the support of locally based platforms. Accounting for such a large proportion of the world’s population, the APAC region’s contribution to the popularity of the OTT video space will allow content creators, providers, and marketers alike to reach their audiences at a higher rate, resulting in exponential growth figures’.

But, as in many cases, responding to this demand it’s a big challenge, especially if we analyze the inflationary content costs in countries such as India, Japan, Korea and Thailand. A more strategic and partnership driven model is key to success as well as forming longstanding co-production and IP partnerships, not only on the documentary field, but also on scripted formats.

As the market continues to expand, driven by Asia’s consumption for TV & film content growth, local companies started to invest from some years now into expansive studios, based upon the box-office recoupment model of one-off, mega-budget productions north of $100 million.

With US and Europe fast maturing and China inaccessible, APAC’s large markets – India, Indonesia, Japan, Korea and Thailand – will be increasingly important to global platforms, said consultancy and research firm Media Partners Asia in its report “Asia Pacific Online Video & Broadband Distribution 2022.”

The report, which covers the AVOD and SVOD sectors and spans China, India, Australasia, Southeast Asia as well as South Korea and Japan, shows the overall industry on course to grow by 16% in the current year to $49.2 billion. SVOD will contribute 50%; user-generated content-driven ad-supported VOD 37%; and premium AVOD, 13%.

China’s Bytedance, operator of Douyin and Tiktok, has the largest video revenue in the region with a 2022 figure close to $7 billion. Indeed, China has three companies in the top five by revenue. MPA ranks the five largest as: Bytedance, YouTube, TencentVideo, Netflix and iQiyi.

Within China, two long-form platforms Tencent Video and iQIYI, and two short-form video players ByteDance and Kuaishou lead. Those four are forecast to capture some 70% of China’s online video revenue in 2022. And China, despite regulatory hurdles and increasing maturity, will remain APAC’s largest single video market. It is forecast to grow at an annual 5% to 2027 with revenues in excess of $30 billion, or 42% of the APAC total. However, China’s video market is “insular and largely closed to international streamers.”

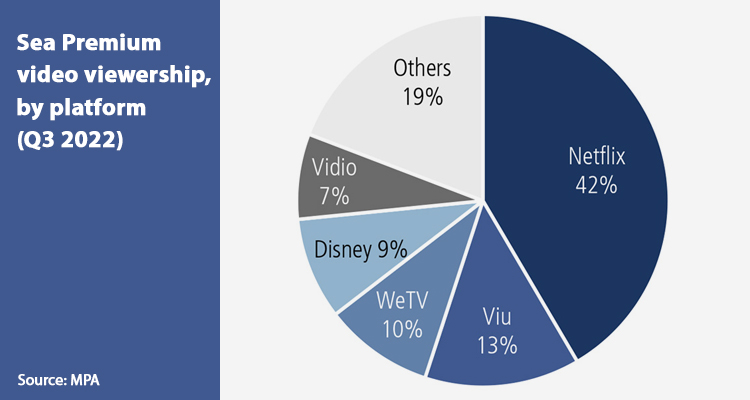

Outside of China, YouTube, Netflix, Disney and Amazon Prime Video have almost 50% of online video revenue in the region. MPA forecasts figures coming in at $5.7 billion, Netflix at $4 billion, Amazon’s Prime Video at $1.4 billion; and Disney at $1.3 billion in 2022.

Japan and Korea are key markets, both for industry growth and for content. Both countries offer high average revenue per customer and high advertising rates, yet online video penetration is far behind Australia or the U.S. Households penetration is 49% for Japan and 42% for Korea. After China, Japan is the region’s largest OTT market by revenue, generating $9.7 billion in 2022. It is forecast to grow to $14.7 billion by 2027.

‘Disney+ and Disney+ Hotstar services are building scale, local content investment and monetization in markets such as Australia, India, Indonesia, and Thailand while also expanding in high ARPU, strong local markets such as Japan. A third of revenues come from India however, where it has recently lost digital rights to the highly successful IPL cricket franchise to Viacom18,’ the report says.

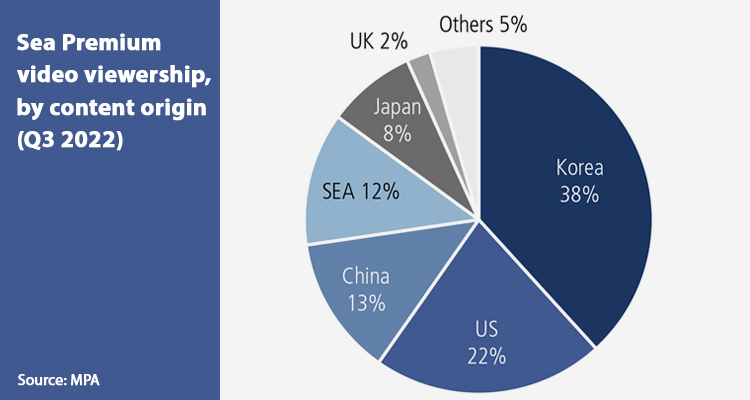

In terms of genre, on TV, drama is generally the most watched genre while variety, including reality, often ranks #2. Movies, kids, and news can be significant drivers of viewership and sports can over-index with top rating TV programs. Viewership of some key TV genres is transitioning to YouTube, where they generate significant classified consumption. Meanwhile with premium online video, approximately 90% of consumption is series, the bulk of which is drama, while movies generate about 10% of viewership. Dramas account for nearly all top titles..