The FAST model continues its interesting expansion, moving from an experimental niche to a central component of the global media landscape. The total number of FAST channels globally increased by approximately 42% from 2023 to early 2025, demonstrating explosive growth outside of North America in markets like the U.K., Germany, and Canada.

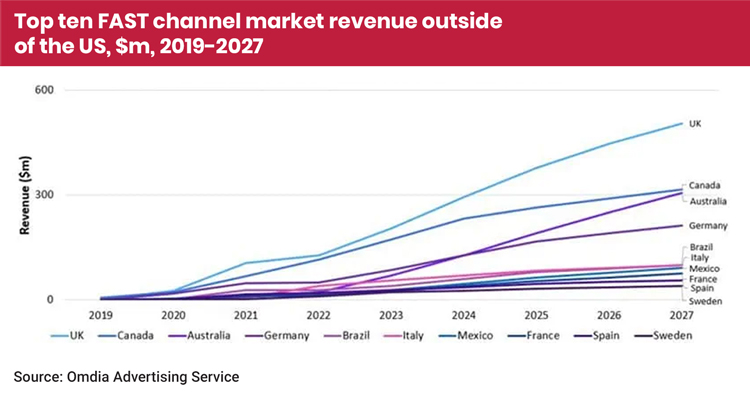

This momentum is driving both impressive revenue and technological change. In 2023, the North American region alone accounted for over 50% of the roughly $8 billion in global FAST revenues. Projections indicate that Europe’s revenue share, which stood at about $1.36 billion in 2023, will rise significantly to approximately $3.74 billion by 2029. Notably, Brazil is expected to become the third-largest FAST market globally by 2029, with revenues projected to nearly triple from $119 million in 2024 to about $303 million.

New market dynamics and content trends

The leading platforms reflect this rapid expansion. Samsung TV Plus demonstrates significant growth, hosting nearly 700 channels in the U.S. by April 2025—more than any competitor—and over 3,500 channels globally. The platform also saw a 30% year-over-year engagement boost in 2025.

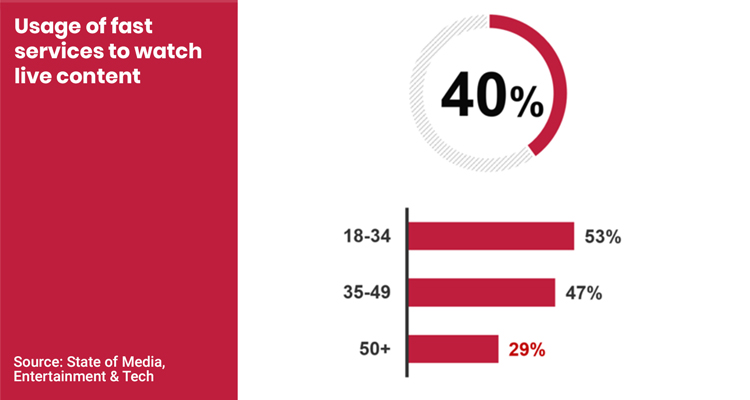

Viewing trends indicate that FAST is moving beyond being a destination for reruns. Only 13.4% of available content was produced before 1990. The key growth areas are currently in sports and reality genres.

Sports-oriented FAST channels surged by more than 105% between mid-2024 and February 2025, reaching 220 dedicated channels. This growth involves real-time streaming of live events, such as FOX‘s free livestream of Super Bowl LIX on Tubi in February 2025, and MLB and Formula 1 races on The Roku Channel.

Reality TV channels experienced even more striking growth, rising by 626%—from 19 to 138 channels—in less than a year between July 2024 and February 2025.

The attention paradox

Despite this financial success, a core challenge remains: audience attention spans have never been shorter, dictated by the pace of platforms like TikTok. While Netflix found viewers often decide on a title within 90 seconds, FAST channels provide «always-on, linear-like» streams, potentially conflicting with audiences trained to demand control over their viewing.

However, this divergence may not represent a conflict but a different use case. FAST serves «lean-back» discovery rather than «lean-forward» choice; viewers tune in for passive, entertaining background content while multitasking, prioritizing companionship over hyper-engagement.

Advertisers must adjust their metrics accordingly, prioritizing ambient engagement over completion rates. Metrics like dwell time and co-viewing households become more relevant than guaranteed full attention.

Another problem has been the abundance of content, which creates a significant challenge for platform usability. Viewers are overwhelmed, as the average FAST service offers over 1,600 channels. In a survey conducted in January 2025, 73% of respondents said they needed multiple streaming apps to find something to watch, and 48% had canceled a service due to poor content discovery.

The core technical failure compounding this is insufficient metadata. According to the “Gracenote FAST Report 2025”, many channels lack basic genre tags, and 43% of programs lack imagery, forcing users to «click through blindly». This problem compromises the entire revenue model: insufficient metadata limits marketers’ ability to align campaigns, despite 75% of CTV ads being bought programmatically.

Artificial Intelligence is emerging as the primary tool to address this data gap. Companies are utilizing machine learning to analyze video files and automatically generate detailed, consistent metadata, which improves viewer recommendations and allows advertisers to access «rich, consistent descriptors» for precision targeting.

AI is also facilitating global expansion through innovative localization tools. For example, AI-Media and Lightning International launched a partnership to integrate live, burned-in captions across FAST channels in more than 50 languages.

Technical improvements

The FAST market is currently defined by rapid experimentation. Recent shifts include Amazon‘s shoppable FAST channel experiments, which merge commerce and content, and Warner Bros. Discovery‘s pivot to license premium legacy shows to FAST ecosystems. The emergence of niche channels—focused on specific genres like news or food—allows brands to cost-effectively reach highly targeted audiences.

However, inefficiencies remain. The programmatic advertising supply chain often involves «daisy-chained SSPs» (multiple supply partners), which confuses buyers and reduces revenue for broadcasters. Furthermore, data opacity makes it difficult for advertisers to accurately calculate ROI across fragmented reporting from platforms like Samsung and Roku. Calls for standardized measurement are growing as a result.

To address these market inefficiencies, companies like View TV are introducing initiatives like FASTNXT (Next Generation FAST). FASTNXT aims to redefine the market by prioritizing transparency, reducing intermediaries to a «One SSP Model,» and delivering real revenue-per-hour-watched (RPH) metrics.

AB