Recent research from Ampere Analysis highlights a stark contraction in children’s and family content commissions by major streaming platforms, with their share dropping from 9% in 2022 and 2023 to just 4% across 2024 and 2025. This strategic pullback is largely attributed to the overwhelming dominance of YouTube among younger demographics, coupled with the complexities of monetizing children’s programming within ad-supported subscription tiers. However, the unprecedented performance of a single original title is now challenging this industry-wide retreat.

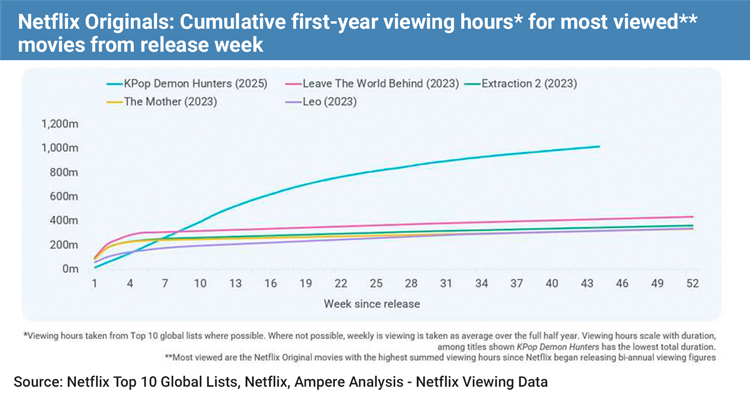

The Sony Pictures Animation production KPop Demon Hunters has officially become the most-watched film in Netflix history, surpassing one billion viewing hours and maintaining a presence in the platform’s global Top 10 charts for a record 44 consecutive weeks. Ampere Analysis data indicates that family-friendly titles of this nature possess a significantly longer viewing lifecycle compared to typical original films. Underscoring this trend, KPop Demon Hunters did not reach its viewership apex until 11 weeks after its initial release.

The success of the animated feature, heavily fueled by the global K-Wave phenomenon and a strong musical core, demonstrates the enduring capacity of high-quality original intellectual property to retain audiences across multiple demographics. This metric is particularly relevant given that 35% of households with children report that kid-friendly content serves as a primary driver for their subscription loyalty, suggesting that SVoD platforms may be underestimating the retention value of premium family features.

Beyond individual platform successes, the broader data reveals a significant divergence in commissioning priorities across the global media industry. While subscription video-on-demand services have significantly retreated from the space, currently holding the smallest share of scripted kids’ greenlights at a mere 13%, traditional public broadcasters remain the primary engine for the sector. According to Ampere, public institutions are responsible for nearly half of all global children’s content orders in 2025, accounting for 47% of the market and underscoring a landscape where traditional entities remain committed to youth content while major streamers increasingly look elsewhere to build their libraries.