Driven by the confinement following the coronavirus pandemic, Gaming industry revenues in 2020 and 2021 were much higher than anticipated at the time. NewZoo‘s Global Games Market Report, claims that the global gaming market generated $184 billion in 2023, representing a year-on-year growth of 0.6%. With around 3 billion gamers worldwide, through 2024 the market could grow at a compound annual growth rate of 8.7%, reaching $218.7 billion. Mobile will contribute to most of this growth, in addition to the new generation of consoles such as the Nintendo Switch successor. As gaming becomes more mainstream and young people get older, the number of gamers will increase across the board.

Thanks to the expansion of technology, new tools, the considerable increase in the quality of content, the professionalization of e-sports, streaming services and niche platforms, the number of global players continues to grow worldwide. NewZoo indicates that this 2023, the number of players grew by 7.3% worldwide, reaching 1470 million in 2023; and going forward, it will continue to grow with a CAGR (2021-2026) of +4.7% to reach 1.66 billion players by the end of 2026. Mordor Intelligence indicates that the gaming market is expected to register a CAGR of 8.94% during 2018-2028; and Satista estimates that by 2027, the global Gaming industry could reach $340 billion.

Next year, the industry is expected to experience further growth as publishers invest in quality that can compete with premium console and PC games. All segments will add new players to the global gaming market as games are developed in the cloud, with multiplayer options and cross-platform compatibility, releases will reach more audiences and increase retention.

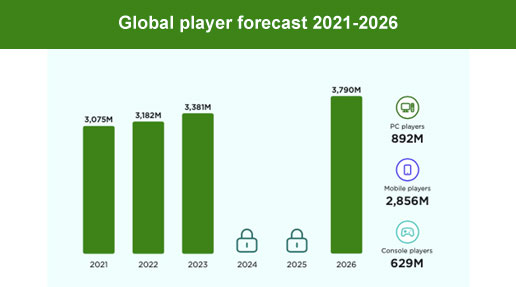

Games are fully integrated into society: As existing players age and new ones join; the number of players will continue to grow. The biggest game-based transmedia releases of 2023, such as the Super Mario Bros movie and The Last of Us series, along with productions in development, will continue to legitimize the industry among non-regular and lapsed gamers. Thus, the number of gamers worldwide will continue to grow with a 2021-2026 CAGR of +4.3% to reach 3.79 billion gamers by the end of 2026.

Asia-Pacific accounts for more than half of the world’s players, thanks to large markets such as India and China and countries with a great love of the game such as Japan and South Korea. North America and Europe account for 20% of players. In relative terms, the less mature markets of the Middle East and Africa (+12.3% year-on-year player growth) and Latin America (+6.1%) will grow the most in 2023. Among the causes, better (mobile) Internet infrastructure, accessible and affordable (mobile) Internet, and the rise of the middle class stand out. The availability of games as an affordable recreational activity, thanks to the free-to-play model and the increase in the population of smartphone users.

Most regions will enjoy healthy gaming revenue growth in 2023. Asia-Pacific is the largest gaming region in 2023, accounting for 46% of global revenues. However, as the region’s revenues will decline -0.8% year-on-year in 2023, Asia-Pacific’s growth lags the rest of the world. This may come as a surprise due to the region’s numerous growth markets. The slower-than-usual pace of growth is due to the Chinese market pulling down the region’s average with its +0.7% year-on-year revenue growth.