A new report, «Key Trends 2025,» from the European Audiovisual Observatory (EAO) reveals a complex picture of the European media landscape, marked by a slowdown in overall growth, a significant shift toward digital platforms, and emerging challenges from artificial intelligence. The report, which provides a pan-European overview of television, cinema, video, and on-demand services, highlights that while some sectors show growth, this is largely failing to keep pace with inflation.

Market and revenue trends

According the EAO, the audiovisual market in the EU grew by 4.3% in 2023, but this growth was outpaced by a 6.4% inflation rate, meaning the market effectively shrank in real terms. The industry’s share of the European Union’s gross domestic product has been in steady decline, dropping from 0.67% in 2014 to 0.59% in 2023. This limited growth is almost entirely attributed to the subscription and transactional VOD segments, as traditional sectors like TV advertising and physical home video are either stagnating or declining. For the first time in 2023, consumer spending accounted for half of all revenues in the European audiovisual sector, up from 44% a decade ago.

Advertising is undergoing a major shift, with internet advertising growing by 6.2% in 2023, reaching €92.2 billion. In contrast, TV advertising expenditure decreased by 3% to €30.7 billion, a level almost identical to 20146. This trend is fueled by increased competition from digital players, including streaming services with ad-supported tiers, and video-sharing platforms like YouTube, which captured 24% of the video advertising market in 2023.

Production and content trends

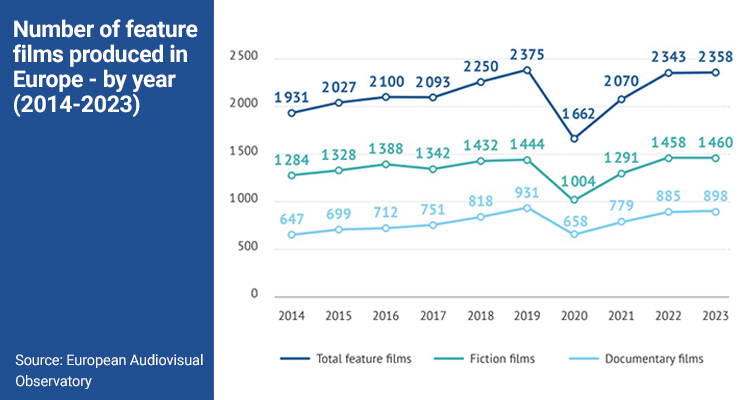

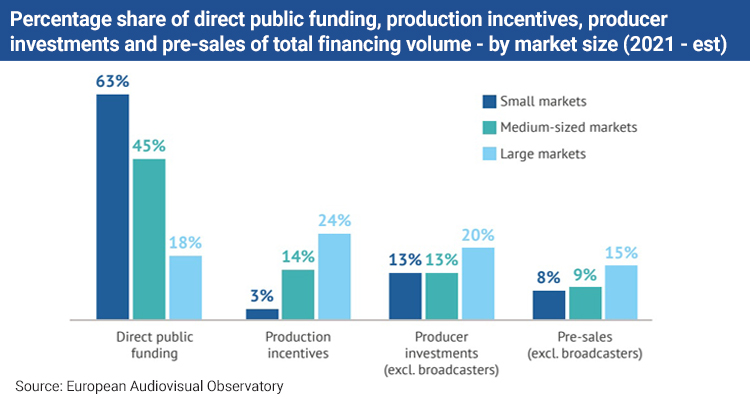

European film production has rebounded to pre-pandemic levels, with an estimated 2358 feature films produced in Europe in 2023. Fiction films reached a new high of 1,460 productions, while documentaries accounted for 898 titles. Italy led in production volume, followed by Spain, France, and the UK. Investment in film production also continued to grow in 2023, rising by 14% compared to 2022. Direct public funding remains the most important financing source for European theatrical fiction films, but production incentives have risen to become the second most significant source.

Conversely, TV fiction production is in decline after a brief post-pandemic return to growth. The number of fiction titles dropped by 6% in 2023 compared to the previous year. Over half of fiction titles were commissioned by public service broadcasters (55%), followed by private broadcasters (31%) and global streamers (14%). Short formats, such as high-end TV series with 3 to 13 episodes, continue to be popular, showing a 105% increase since 2015.

The report also highlights a growing reliance on adaptations of books and other media. From 2015 to 2022, 12% of all audiovisual fiction works in Europe were adaptations. Streamers offer a higher proportion of adaptations (19%) than private (13%) or public (11%) broadcasters.

Digital and streaming landscape

The organization called the European audiovisual sector as ‘vibrant but heavily influenced by US players’, where nine out of the top 10 most widespread TV and VOD groups in Europe are US-based. Major brands like Warner Bros. Discovery, Disney, Netflix, and Amazon have a significant presence across multiple European markets. Despite this, local media services still have significant weight, with 42% of TV channels in Europe being regional and local services.

SVOD usage is highly concentrated, with Netflix, Prime Video, and Disney+ accounting for 85% of viewing time. European works make up 30% of SVOD viewing time, though this figure varies significantly by country. The report also found that European films are under-consumed on SVOD platforms compared to their catalogue presence. In contrast, European films perform better in cinemas than on TV or SVOD when only theatrical films are considered.

AI and regulation

The report addresses the need for ‘AI literacy skills’ to help the public critically engage with AI-driven technologies. It notes that AI-enhanced disinformation could further undermine trust in public and government information. The challenges posed by AI, such as deep fakes and algorithmic bias, require critical thinking and a multi-stakeholder approach to education involving experts, journalists, and developers. The revised Audiovisual Media Services Directive (AVMSD) provides a broad framework for regulating influencers, but many EU countries still lack a specific legal definition of the term.