The European Audiovisual Observatory has published its Key Trends 2026 report, providing a comprehensive, data-driven analysis of the European audiovisual sector. The findings track crucial structural shifts across the creative economy, from record-setting film production metrics to deep transformations in consumer streaming preferences, regional financing, and global market positioning.

According to the whitepaper, the European audiovisual ecosystem generated approximately €142 billion in total revenues in 2024. Direct consumer spending—a category encompassing SVoD renewals, traditional pay-TV, theatrical box office receipts, and home video purchases—served as the primary economic engine, contributing over half of the market’s total value at €72 billion.

Concurrently, the financing matrix for local content is undergoing rapid evolution, heavily influenced by global streaming platforms. Driven by a combination of strict regulatory incentives and an accelerating international demand for localized narratives, global SVoD services have significantly scaled their investments. The platforms’ share of total spending on original European content surged from a modest 8% in 2020 to 24% in 2024, cementing their role as critical financial stakeholders in the region’s production pipeline.

Record production output vs. episodic streaming dominance

On the supply side, European film production achieved an unprecedented milestone. In 2024, the sector reached a historic peak of 2,523 feature films produced across 36 distinct regional markets. This volume confirms a robust post-pandemic recovery and sustained expansion, with growth evenly distributed across both fiction features and documentary formats. Furthermore, average production budgets continued an upward trajectory across the majority of European territories.

However, a stark contrast emerges when analyzing how content is consumed in the digital space. The report highlights a profound imbalance in consumer engagement on streaming networks:

- TV Series Consumption: Accounts for a dominant 78% of total viewing time on SVoD platforms.

- Feature Film Consumption: Attracts just 22% of viewer engagement.

This breakdown underscores the degree to which episodic, multi-part storytelling has become the definitive format driving the modern streaming economy, presenting unique monetization and distribution challenges for traditional feature-length cinema.

The scale gap in global competition

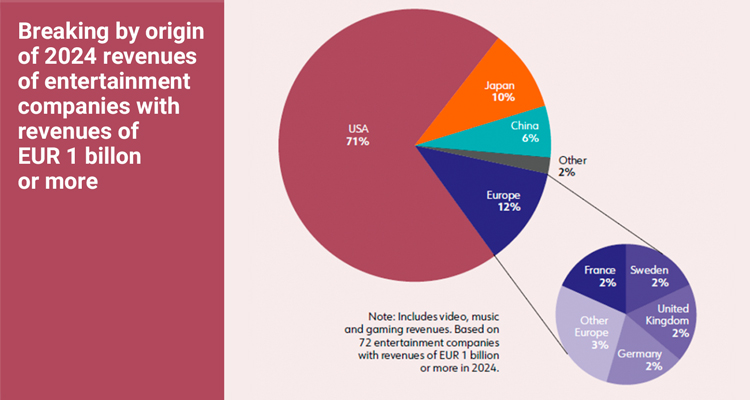

Despite a vibrant production infrastructure and substantial internal revenues, European media companies continue to face a significant scale gap on the international stage. Europe represents a mere 12% of the aggregate revenues generated by the world’s leading entertainment conglomerates.

The global market remains heavily dominated by US-based players. This landscape is mirrored within Europe itself, where major global tech and entertainment platforms—most notably Netflix, YouTube, and Meta—have successfully positioned themselves among the top audiovisual operators inside the European market, shifting the competitive dynamics for native broadcasters and media groups.