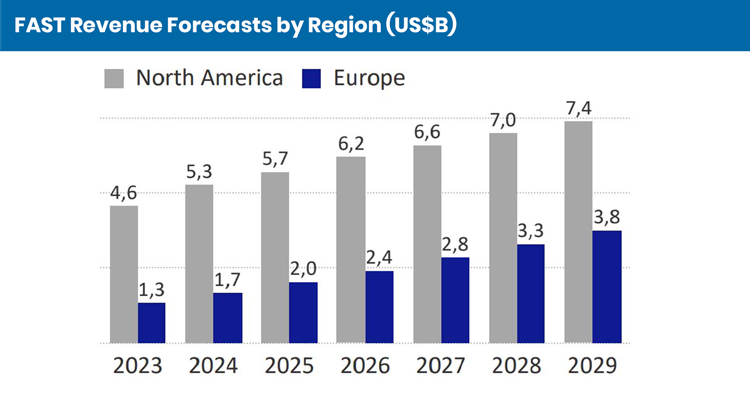

The European FAST market has officially exited its experimental phase and entered a period of rapid maturation and correction. According to the latest whitepaper released by the FAST4EU consortium and 3Vision, Europe is projected to capture 22% of the global FAST market by 2029, up from 17% currently.

While the United States remains the dominant force, the European landscape is evolving differently, driven by a surge in high-quality local content, the entry of major Tier 1 broadcasters, and a ruthless culling of underperforming channels.

The shift from quantity to quality

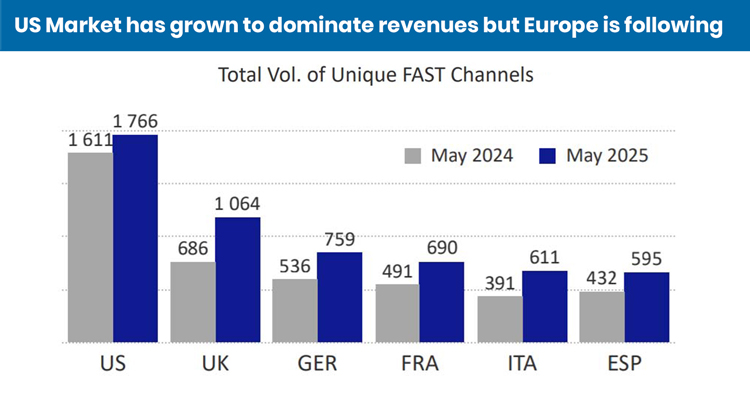

The ‘Wild West’ era of launching any available library content is over. The report highlights that over 600 channels were launched across Europe in the last 18 months. However, unlike the early years dominated by aggregators, 55% of these recent launches came from ‘Tier 1 Owners’—major studios, national broadcasters, and leading brands—signaling a decisive shift toward premium programming.

This flight to quality is best exemplified by the explosion of ‘Single IP’ channels—streams dedicated to a single brand or show, such as Masterchef or Narcos. These channels accounted for 45% of all new launches in the EU5 region (UK, France, Germany, Italy, Spain) between July 2024 and July 2025.

As platforms like Samsung TV Plus, Pluto TV, and LG Channels prioritize user experience, they are aggressively delisting channels that fail to perform. The report reveals a stark statistic: across the top five European markets, an average of 29% of unique channels have been dropped from at least one platform over the last year.

‘As the market continues to mature, platforms will be required to remove under-performing channels in favor of the newer (and higher quality) launches’, the report states. This churn is particularly high in competitive markets like France, where 77% of channels saw some form of removal or rotation, and the UK at 72%.

Local content as the key differentiator

Success in Europe relies heavily on ‘deep localization’. The report emphasizes that while US studios are entering the market at a brisk pace, European broadcasters are in a strong position due to their hold on key local content.

However, monetization remains a complex hurdle. The report notes significant variances in CPMs across the continent. For example, entertainment channel CPMs can range from as low as €8 in Italy to €18 in the UK, highlighting the fragmented nature of the European advertising landscape.