In 2025, US studios continued the complex balancing act of feeding their own D2C platforms while actively targeting lucrative content sales in an increasingly competitive streaming market. A newly released whitepaper by 3Vision, revealed significant shifts in how studios are windowing their content, highlighting a massive pivot towards second-window licensing and a reaffirmed commitment to the traditional theatrical release.

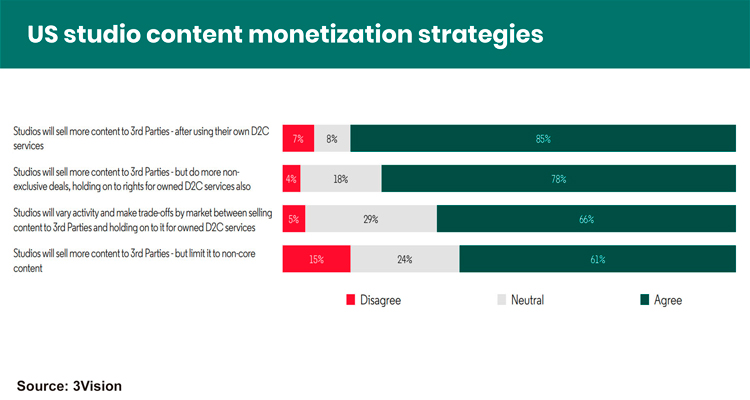

The era of strict vertical integration—where studios hoarded all content exclusively for their own streaming services—appears to be softening. According to the report, 85% of industry respondents agreed that studios will sell more content to third parties after it has premiered on their owned D2C services. Furthermore, 78% of those surveyed anticipate an increase in non-exclusive licensing deals, allowing studios to retain rights for their own platforms while simultaneously generating third-party revenue.

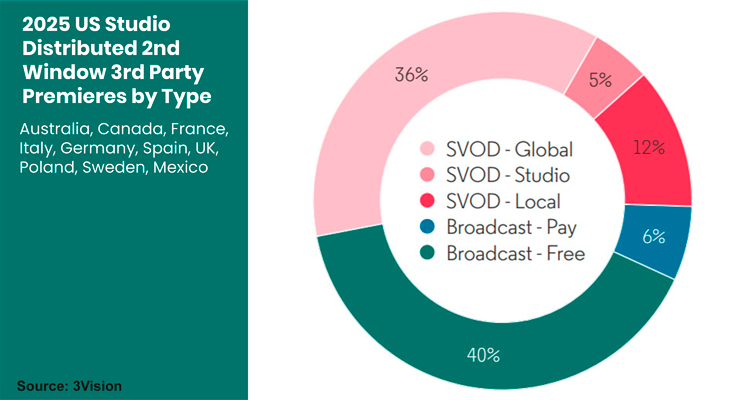

This second-window content is overwhelmingly skewing towards broadcast television. Free TV accounted for 40% of US Studio distributed second-window, third-party premieres in 2025, while Global SVOD platforms secured 36% of these premieres.

Broadcasters are highly receptive to this influx of content. The report notes that 68% of respondents believe Free TV will license more former SVOD originals. However, to secure these sales, buyers are demanding more flexibility; 59% of respondents agree that studios must start granting more comprehensive rights during second windows, specifically including «boxset» (full season) rights. The report highlights that basic catch-up TV offers that omit boxset availability are now considered an exception in the current market.

While the broader market is opening up, certain streaming giants remain outliers. Only 39% of respondents believe Apple will start selling more of its original content to third parties. The report suggests this reluctance may be tied to the reality that Apple‘s previous sales have often been accompanied by a weak set of adjacent digital rights.

Additionally, the industry remains deeply divided on the value of acquiring content that originated on Netflix. A third of the respondents expressed that second windows following a Netflix premiere are not desirable, holding the view that a show’s popularity and appeal are significantly diminished after reaching Netflix’s massive global audience during its first window.

In the film sector, the digital-first approach has taken a backseat to the box office. When asked to rank the various windows of release by importance and value, respondents overwhelmingly favored the Domestic Theatrical window, giving it an average score of 7.98 out of 10, with 36% ranking it as their absolute top priority. International Theatrical followed closely with a score of 7.61. Conversely, the Free TV movie window slipped to the lowest position (5.91), falling behind Library content, Pay-Two, and transactional video-on-demand (TVOD).

Despite the clear value of theaters, the major studios are deploying highly divergent windowing timelines:

- Disney has grown increasingly protective of its theatrical exclusivity, pushing back all premiere windows for its titles since 2023.

- Universal has signaled its intention to grant movies more time in theaters before moving them to Premium Video on Demand (PVOD), a shift away from the typical 35-day PVOD window it utilized over the previous two years.

- Warner Bros. Discovery, in stark contrast, has continued to condense its release timelines. In 2025, Warner Bros. sped up its transition windows, bringing films to PVOD in just 35 days, TVOD in 44 days, and the Pay-One window in 75 days.